Coal Age Magazine - For more than 100 years, Coal Age has been the magazine that readers can trust for guidance and insight on this important industry.

Issue link: https://coal.epubxp.com/i/975717

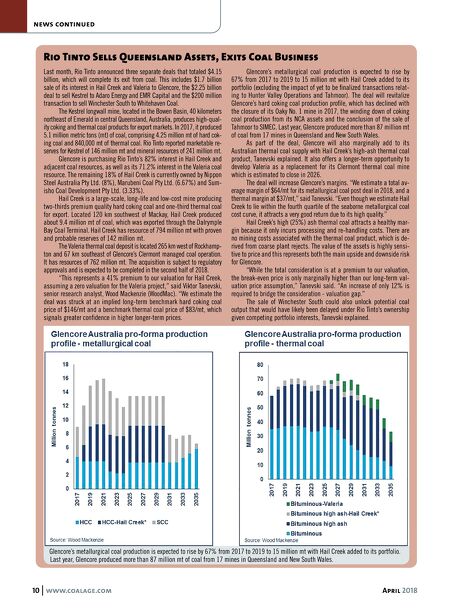

10 www.coalage.com April 2018 news continued Rio Tinto Sells Queensland Assets, Exits Coal Business Last month, Rio Tinto announced three separate deals that totaled $4.15 billion, which will complete its exit from coal. This includes $1.7 billion sale of its interest in Hail Creek and Valeria to Glencore, the $2.25 billion deal to sell Kestrel to Adaro Energy and EMR Capital and the $200 million transaction to sell Winchester South to Whitehaven Coal. The Kestrel longwall mine, located in the Bowen Basin, 40 kilometers northeast of Emerald in central Queensland, Australia, produces high-qual- ity coking and thermal coal products for export markets. In 2017, it produced 5.1 million metric tons (mt) of coal, comprising 4.25 million mt of hard cok- ing coal and 840,000 mt of thermal coal. Rio Tinto reported marketable re- serves for Kestrel of 146 million mt and mineral resources of 241 million mt. Glencore is purchasing Rio Tinto's 82% interest in Hail Creek and adjacent coal resources, as well as its 71.2% interest in the Valeria coal resource. The remaining 18% of Hail Creek is currently owned by Nippon Steel Australia Pty Ltd. (8%), Marubeni Coal Pty Ltd. (6.67%) and Sum- isho Coal Development Pty Ltd. (3.33%). Hail Creek is a large-scale, long-life and low-cost mine producing two-thirds premium quality hard coking coal and one-third thermal coal for export. Located 120 km southwest of Mackay, Hail Creek produced about 9.4 million mt of coal, which was exported through the Dalrymple Bay Coal Terminal. Hail Creek has resource of 794 million mt with proven and probable reserves of 142 million mt. The Valeria thermal coal deposit is located 265 km west of Rockhamp- ton and 67 km southeast of Glencore's Clermont managed coal operation. It has resources of 762 million mt. The acquisition is subject to regulatory approvals and is expected to be completed in the second half of 2018. "This represents a 41% premium to our valuation for Hail Creek, assuming a zero valuation for the Valeria project," said Viktor Tanevski, senior research analyst, Wood Mackenzie (WoodMac). "We estimate the deal was struck at an implied long-term benchmark hard coking coal price of $146/mt and a benchmark thermal coal price of $83/mt, which signals greater confidence in higher longer-term prices. Glencore's metallurgical coal production is expected to rise by 67% from 2017 to 2019 to 15 million mt with Hail Creek added to its portfolio (excluding the impact of yet to be finalized transactions relat- ing to Hunter Valley Operations and Tahmoor). The deal will revitalize Glencore's hard coking coal production profile, which has declined with the closure of its Oaky No. 1 mine in 2017, the winding down of coking coal production from its NCA assets and the conclusion of the sale of Tahmoor to SIMEC. Last year, Glencore produced more than 87 million mt of coal from 17 mines in Queensland and New South Wales. As part of the deal, Glencore will also marginally add to its Australian thermal coal supply with Hail Creek's high-ash thermal coal product, Tanevski explained. It also offers a longer-term opportunity to develop Valeria as a replacement for its Clermont thermal coal mine which is estimated to close in 2026. The deal will increase Glencore's margins. "We estimate a total av- erage margin of $64/mt for its metallurgical coal post deal in 2018, and a thermal margin at $37/mt," said Tanevski. "Even though we estimate Hail Creek to lie within the fourth quartile of the seaborne metallurgical coal cost curve, it attracts a very good return due to its high quality." Hail Creek's high (25%) ash thermal coal attracts a healthy mar- gin because it only incurs processing and re-handling costs. There are no mining costs associated with the thermal coal product, which is de- rived from coarse plant rejects. The value of the assets is highly sensi- tive to price and this represents both the main upside and downside risk for Glencore. "While the total consideration is at a premium to our valuation, the break-even price is only marginally higher than our long-term val- uation price assumption," Tanevski said. "An increase of only 12% is required to bridge the consideration - valuation gap." The sale of Winchester South could also unlock potential coal output that would have likely been delayed under Rio Tinto's ownership given competing portfolio interests, Tanevski explained. Glencore's metallurgical coal production is expected to rise by 67% from 2017 to 2019 to 15 million mt with Hail Creek added to its portfolio. Last year, Glencore produced more than 87 million mt of coal from 17 mines in Queensland and New South Wales.